Ak underwriting field guide final

2011

ODS Alaska Health Plan, Inc. Underwriting Field Guide

for Producers

For state of Alaska individual health benefit plans

The ODS Alaska Underwriting Field Guide is designed to assist the producer in submission of individual and family health benefit plan applications to ODS Alaska underwriters. Adherence to these guidelines will help you and your clients complete applications correctly and thoroughly, thereby reducing processing time in the Underwriting department.

Producers must be appointed with ODS Alaska before submitting an application. It is the producer's responsibility to be thoroughly familiar with Alaska regulations governing these products.

The guidelines stated herein illustrate ODS Alaska's probable actions for many conditions. The guidelines are not binding and are subject to change without notice at ODS Alaska's sole discretion; however, every attempt will be made to keep producers informed of any changes in a timely manner.

ODS Alaska individual health benefit plans are not guaranteed issue for applicants age 19 and older. Only ODS Alaska underwriters make a final decision to accept or reject an individual; producers have no authority to bind or guarantee coverage.

AKFieldguide.2011

Table of Contents

Prior coverage . 4

Employer sponsorship . 4

Acceptable ages . 4

Application submission . 4

Residence requirements . 5

Effective dates . 5

Reinstatement . 6

Intentional fraud or misrepresentation . 6

Pre-existing conditions . 6

ACHIA and ACHIA-FED. 6

Applicant appeal options . 7

Declinable conditions . 8

Underwriting process .10

Co-morbidity factors .10

Prescription/over-the-counter medications .10

Incomplete applications .10

Build charts .11

Common conditions and probable underwriting actions .13

First month's premium .17

Policy delivery .17

Incomplete application and follow-up process .18

ODS Alaska individual application checklist for paper applications .19

AKFieldguide.2011

Prior coverage

If prior coverage is in existence, it is imperative that applicants be cautioned to keep their coverage active until notified by ODS Alaska of their acceptance. Failure to do so may result in loss of coverage if ODS Alaska declines the application.

Employer sponsorship

ODS Alaska individual products are not sold to employers. No employer-sponsored coverage is allowed. Consequently, only personal checks will be accepted with the application. Business or employer checks will be returned and the application will be pended for 15 days awaiting a personal check.

Acceptable ages

Applications for persons under age 19 will be considered for coverage only when applying with parents or guardians on a family application. If coverage for persons under age 19 was terminated previously from the family policy, they can only apply during the open enrollment from December 1st to December 31st of each year to be added back to the family policy.

A newborn child of the insured or an insured dependent child can be added to the policy within 31 days of the date of birth without undergoing medical underwriting. An existing insured's newly adopted child or child placed for adoption can be added to the policy within 31 days of the date of adoption or placement without undergoing medical underwriting. If the addition causes a change in premium, the insured must submit a change form to add the child within 31 days of birth, adoption or placement for adoption along with (when applicable) proof of legal guardianship for a grandchild if the newborn's parent is not enrolled in the policy or legal proof of the adoption or placement. To receive the form or for questions, please contact our Individual Billing and Eligibility department by phone at 1-800-852-5195, ext. 3384, or 503-265-5696, or email [email protected]. Application for these new dependents can also be submitted subsequently for a later effective date.

Adult dependents of an applicant are eligible to be covered under their parents' policy until their 26th birthday.

Application submission

Online applications are available by visiting the ODS Alaska website at www.deltadentalak.com/agents under Online Applications, where detailed instructions are provided for the producer link and online application submission. Online submissions without a producer can be accessed through our website at www.deltadentalak.com by selecting "Looking for a health plan."

AKFieldguide.2011

Paper applications are available in PDF on our website or from ODS Alaska by contacting the Individual Sales department at 907-278-2626 or 888-374-8910. Paper applications must be completed in either blue or black ink and sent to:

ODS Alaska Individual Underwriting 601 W. 5th Ave., Suite 510 Anchorage, AK 99501

The applicant's home address must be the applicant's physical address. A P.O. Box is not acceptable as a primary address, but may be used for billing purposes.

The answers to the application questions must be accurate and complete. If more space is needed, a separate sheet of paper providing more detail may be submitted with the application, providing it is signed and dated by the applicant. Any changes must be crossed out and initialed by the applicant.

If any questions are not answered, the application will be delayed until the missing information is received. Please ensure that each application is correct and complete before submission. If the application is incomplete and we do not receive the missing information in a timely manner, the application will be closed and a new application, including the missing information and a new, dated signature, will be required.

Trial and prescreen applications cannot be accepted. Approved applicants do have a 10-day free look period for review of the policy. The approved applicant may request to cancel his or her policy during this period as though it had never been effective and receive a full refund of the initial premium, assuming no claims have been paid.

Residence requirements

All applicants must be residents of the state of Alaska and/or reside in specific service areas of the plan. If any enrolled child(ren) resides outside the service area, we will extend benefits for treatment of an illness or injury and preventive healthcare as if rendered by a participating physician or provider. Out-of-area dependents must access benefits within a 50-mile radius of their residence for the in-network benefit level to apply.

Effective dates

Upon underwriting approval, the underwriter will assign an effective date for the first or the 15th of the month. To be considered for an effective date of the first of a month, an application must be received 10 days prior.

AKFieldguide.2011

An application is considered a reinstatement if the prior individual policy was terminated within the last 60 days. ODS Alaska must collect previously unpaid premiums at the time of reinstatement. The applicant must also choose EFT (electronic funds transfer) as the future billing method. If an applicant would like to reinstate his or her policy, please contact our Individual Billing and Eligibility department by phone at 1-800-852-5195, ext. 3384, or 503-265-5696, or email [email protected].

Intentional fraud or misrepresentation

If fraud or intentional misrepresentation of material is discovered, the policy may be subject to rescission. Fraud or intentional material misrepresentation exists when an applicant misrepresents medical history, residence or other significant factors that, had they been made known at the time of application, would have resulted in the underwriter modifying or declining coverage. If this occurs, coverage will be deemed to never have been in force and all premiums, minus the costs of any claims paid, will be refunded. ODS Alaska will require the producer to return any commissions that had been paid.

Pre-existing conditions

ODS Alaska does not pay toward a pre-existing condition for members over age 18, even if the pre-existing condition worsens or recurs during the first 12 months of the term of the policy. Existing creditable coverage can reduce the 12-month period if an individual's most recent period of creditable coverage is still in effect on the date of enrollment or ended within 90 days of the effective date of coverage. Creditable coverage followed by a break in coverage exceeding 90 days will not reduce the pre-existing conditions waiting period. Each day of creditable coverage will reduce the 12-month period by one day. To apply the credit, ODS Alaska requires the submission of a certificate of creditable coverage provided by the previous insurer to the insured.

ACHIA and ACHIA-FED

ODS Alaska adheres to all of HIPAA's confidentiality guidelines. You can view these at www.deltadentalak.com/hipaa/index.shtml.

The Alaska Comprehensive Health Insurance Association (ACHIA) and ACHIA-FED (federal pool) are default providers for individuals who are declined by an individual insurer. Federally defined eligible individuals are not subject to any pre-existing conditions limitations. ACHIA/ACHIA-FED may give pre-existing credit for other individuals who apply within 31 days after an involuntary termination from another medical plan or policy. People who have certain conditions as defined by ACHIA may automatically qualify without being declined by an individual insurer. The conditions listed by ACHIA for

AKFieldguide.2011

automatic coverage are the same conditions that are declined by ODS Alaska. Producers should follow the ACHIA automatic conditions listed in the ACHIA application. Applications should not be submitted if the applicant has a condition on the ACHIA list. To view a list of ACHIA conditions, go to: www.achia.com/qualify.asp.

Applicant appeal options

If an applicant does not agree with an ODS Alaska underwriting decision to decline coverage, he or she, or an authorized representative, has the right to file an appeal with ODS Alaska by providing a written request within 180 calendar days following receipt of the declination letter.

A Complaint and Appeal Form is available at http://odsalaska.com/docs/grievance_form.pdf or by calling our Individual Sales department at 907-278-2626 or 888-374-8910.

The Complaint and Appeal Form is not required, as long as the written request includes information regarding the declination. The applicant has the right to be represented in the appeal process by any person of his or her choosing, including an attorney, but representation is not required.

All information the applicant wishes ODS Alaska to consider as part of the appeal must be submitted with the appeal request. The applicant may also present additional evidence and testimony to support the request. This information will be reviewed by persons not involved in our previous decision. We will review the information and respond within 30 days.

Send appeals by mail or fax to:

ODS Alaska Attention: Appeal Unit 601 S.W. Second Ave.

Portland, OR 97204 Fax: 503-412-4003

The applicant has the right to receive, upon request and free of charge, a copy of all documents relevant to this denial. For receipt of those documents or questions regarding filing an appeal, please contact our Individual Sales department by phone at 907-278-2626 or 1-888-374-8910.

In addition, the applicant or authorized representative has the right to file a complaint or seek assistance from the Alaska Division of Insurance by calling 907-269-7900, sending an email to [email protected], or writing to the Consumer Services Section at 550 W. 7th Ave., Suite 1560, Anchorage, AK 99501-3567.

AKFieldguide.2011

Declinable conditions

For applicants age 19 and over, ODS Alaska declines those conditions listed on the ACHIA application. ODS Alaska may also decline some additional conditions that are not on the ACHIA list, as indicated below. An applicant must submit an application in order to receive a formal declination and be eligible to apply for ACHIA, if the condition is not listed as an ACHIA condition.

ODS Alaska's list of declinable conditions includes, but is not limited to, the following:

Cancer/metastatic cancer

Adams-Stokes syndrome

Addison's disease

Adrenal insufficiency

Charcot-Marie-Tooth disease

Alcohol/chemical dependency

Chronic obstructive pulmonary

Alzheimer's disease

Chronic pancreatitis

Cirrhosis of the liver

Amyotrophic lateral sclerosis

Congestive heart failure/

Analgesic abuse nephropathy

Coronary insufficiency/occlusion/

Ankylosing spondylitis

Anorexia/bulimia

Aortic valve insufficiency

Cushing's disease

Aortic valve stenosis

Aplastic/sickle cell/splenic anemia

Arnold-Chiari malformation

Arteriosclerosis obliterans

Artificial heart valve

Ehlers-Danlos syndrome

Barrett's esophagus

Fragile X syndrome

Becker muscular dystrophy

Friedreich's disease

Behcet's syndrome

Gastric bypass surgery

Berger's disease

Gaucher's disease

Bipolar disorder

Blood coagulation disorder

Burkitt's lymphoma

Heart enlargement

AKFieldguide.2011

Hodgkin's disease

Polycystic kidney

Huntington's chorea

Polycystic ovarian syndrome

Posterolateral sclerosis

Hypertensive renal disease

Pregnancy (current)

Intermittent claudication

Progressive systemic sclerosis

Ischemic heart disease

Psychotic disorders

Pulmonary fibrosis

Lead poisoning (cerebral)

Rheumatoid arthritis

Sickle cell anemia

Sjogren's syndrome

Marfan's syndrome

Splenic anemia/True Banti's syndrome

Mental retardation

Mixed connective tissue disease

Motor or sensory aphasia

Multiple or disseminated sclerosis

Tabes dorsalis/locomotor ataxia

Muscular atrophy/dystrophy

Thalassemia/Cooley's or Mediterranean

Myasthenia gravis

Topectomy and lobotomy

Obesity (morbid)

Transient ischemic attack

Open heart surgery

Paraplegia/quadriplegia

Ulcerative colitis

Parkinson's disease

Von Recklinghausen's disease

Von Willebrand disease

Peripheral arteriosclerosis

Wilson's disease

Pituitary gland disorders

The final decision regarding coverage rests with the underwriter and the ODS Alaska medical director.

AKFieldguide.2011

Underwriting process

Applications are reviewed in the order they are received. ODS Alaska underwriters review the application, obtain medical records when necessary, and may contact the producer or applicant if additional information is required. ODS Alaska's target turnaround time for underwriting decisions is within 10 business days of receipt, if additional information is not required. Most decisions are to accept or to decline to offer coverage to an applicant. Offers may be made to other family members when one family member may be uninsurable. In some cases, the underwriter may be able to offer coverage if the applicant agrees to accept a higher deductible or waiver for a pre-existing condition. Please see examples of disorders and the probable action under "Common conditions and probable underwriting actions."

Co-morbidity factors

Multiple risk factors can affect risk in an adverse way. For example, an applicant with high blood pressure that is controlled may be an acceptable risk; however, if he or she is a smoker and also has high cholesterol, the applicant may be declined. The final decision may deviate from guidelines when multiple conditions exist.

All applicants age 19 and over must indicate all past (last 10 years) and current prescription and over-the-counter medications. Each medication must be explained in Section 7 with the condition(s) being treated. If there is no condition indicated, ODS Alaska will return the application as incomplete.

Incomplete applications

ODS Alaska has access to prior ODS Alaska claims. If a prior ODS Alaska member, whether on a group or individual plan, submits an application and claims history that was not originally indicated on the application is found, the application will be considered incomplete. Underwriting may return the application for further details regarding the applicant's medical history.

All questions in Section 6 must have a "yes" or "no" answer. If any questions are left unmarked, the application will be considered incomplete. If there are any "yes" answers, they must be addressed in Section 7 with complete medical history, including: question number, start and end dates, condition, treatment, resolution and physician/hospital.

Underwriting requires a new signature in the authorization section when an application is returned as incomplete; this ensures we can continue to process the application.

AKFieldguide.2011

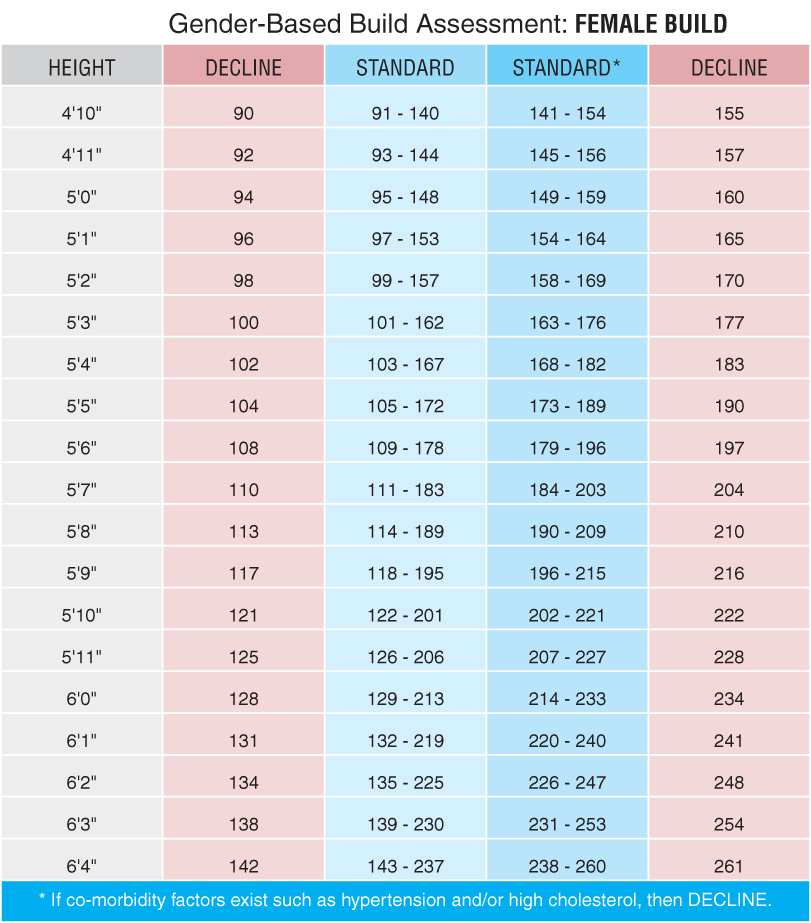

Build charts

ODS Alaska underwriters use height and weight to determine if a person is insurable. The minimums and maximums are noted below; any build outside these limits is not insurable. Please measure the height and weight of all applicants age 19 and over. Estimates and guesses are not sufficient.

AKFieldguide.2011

AKFieldguide.2011

Common conditions and probable underwriting actions

In some situations, ODS Alaska may decide to offer coverage with a higher annual deductible or a waiver on a pre-existing condition, rather than declining the application. A limited number of examples of common conditions are noted below. An application must be submitted in order for the applicant to be formally declined.

"Subject to deductible/waiver" indicates some conditions may limit plan choices to higher deductibles. Approval is not guaranteed, but upon underwriting review a downgrade or a waiver on a pre-existing condition may be offered instead of a decline.

CONDITION PROBABLE ACTION

ACNE

A skin disorder. Severe form may require prescription

medication.

Mild, treated with topical ointments only

Moderate, treated with oral meds, not Accutane

Subject to deductible/waiver

Severe or currently on Accutane

ALLERGIES OR ALLERGIC RHINITIS

A seasonal or perennial allergy to dust and pollens.

Seasonal, no asthma or inhaler use

Perennial or with asthma

Subject to deductible/waiver

Undergoing desensitization treatments

Subject to deductible/waiver

ASTHMA

Difficult breathing due to allergens.

Mild, seasonal, no hospitalizations

Subject to deductible/waiver

Perennial, no hospitalizations

Subject to deductible/waiver

Severe or with hospitalizations

BACK AND NECK STRAIN OR SPRAIN

Back and neck muscle pain due to overexertion

One episode, fully recovered under one year

One episode, fully recovered over one year

Multiple episodes within three years, no disc disorder Subject to deductible/waiver Multiple episodes over three years, no disc disorder Standard With spinal manipulation, no more than six per year Standard With spinal manipulation, more than six per year Subject to deductible/waiver Over one year since last manipulation

AKFieldguide.2011

CATARACT

An opacity of the lens of the eye.

Un-operated: congenital, traumatic and senile

Operated: congenital and traumatic

Operated: senile, recovered under one year

Operated: senile, recovered over one year

DIVERTICULITIS/ DIVERTICULOSIS

Diverticulosis is a pouch in the intestine

Diverticulitis is inflammation of the pouch

Diverticulosis, found incidentally, asymptomatic

Diverticulitis un-operated, one attack, recovered; over two years since recovery

Multiple attacks

Diverticulitis, operated, recovered over two years

GERD

Gastroesophageal reflux disorder. Acid reflux.

Mild, treated with non-prescription medication

Treated with prescription medication

Subject to deductible/waiver

HEADACHES OR MIGRAINES

Mild, occasional episodes

Severe or frequent, definite diagnosis, not disabling

Subject to deductible/waiver

GENITAL HERPES

A viral infection of the genitals.

0–6 months since infection

Over 6 months since infection, controlled

Subject to deductible/waiver

HEPATITIS

An acute or chronic inflammation of the liver

Hepatitis A, E: over six months since recovery

Hepatitis B: over one year since full recovery

Hepatitis C, D, G

AKFieldguide.2011

HERNIA

A hernia is a protrusion of a loop or knuckle of an organ

or tissue through an abnormal cavity.

Present: incisional, inguinal,

umbilical, scrotal, ventral

Surgical resolved: incisional, inguinal, umbilical, scrotal, ventral

Subject to deductable/waiver

HYPOTHYROIDISM

Inadequate production of thyroid hormone.

Adequately treated with thyroid supplements

Not adequately treated

IRRITABLE BOWEL SYNDROME

A non-ulcerating irritation of the intestines.

Definite diagnosis, not on prescription medication:

one episode, less than one year since last attack

Subject to deductible/waiver

One episode, over one year since last attack

KIDNEY STONE(S)

Abnormal mineral collections (mainly calcium) that form

in the kidney, ureter or bladder

History of one attack, within last three years

History of one attack, over three years

History of multiple attacks

KNEE DISORDERS

Arthritis of knee or knee replacement

ACL or meniscus tears, fractures, un-operated

Operated over one year since surgery, recovered

OSTEOARTHRITIS

A degenerative arthritis commonly associated with aging.

Minimal, no interference with function,

non-weight-bearing joint

Moderate, some interference with function or on prescription medication, non-weight-bearing joint

Subject to deductible/waiver

Severe or affecting hips, knees or ankles

AKFieldguide.2011

SLEEP APNEA

Cessation of breathing during sleep. Two types —

obstructive: due to blockage of the airway;

central (mixed): due to a brain stem disorder.

Obstructive apnea using CPAP, not overweight

Subject to deductible/waiver

Operated, recovered, no treatment required

Central or mixed apnea

Some conditions will require additional information and may be submitted with the original

application, as indicated below. Submitting this information with the application will assist

the underwriting process.

COSMETIC SURGERY/IMPLANTS

Please indicate the type of implant.

CHOLESTEROL, ELEVATED

Please give total cholesterol, HDL, LDL and

Elevated lipids in the blood

triglyceride readings.

Please provide the most recent reading from

Increase in blood pressure

a doctor's office.

MENTAL/ EMOTIONAL CONDITION/

Subject to underwriting review. Please

DEPRESSION AND THERAPY

indicate any mental health drugs. If therapy or counseling is indicated, include the most recent date of service.

OSTEOPOROSIS OR OSTEOPENIA

Please submit latest DEXA scan results.

A decrease in bone mass

PAP SMEARS

If past history of abnormal results, two

A laboratory smear of the cervix

normal Pap smears required.

SKIN TUMORS

Please submit pathology report.

Growths or neoplasms of the skin

SURGICALLY REPAIRED

Please indicate if hardware is present.

BONE FRACTURES

AKFieldguide.2011

First month's premium

In the case of direct bill, the producer is responsible for collecting the full first premium. All checks should be drawn on a personal bank account, dated with the same date the application is signed, and made payable to "ODS Alaska." Checks made payable to an agency will be returned.

For automatic bank withdrawal from a personal bank account only, a copy of a voided personal check must be submitted with the application. First premium withdrawal will occur immediately on approval. After the first premium withdrawal, billing occurs on the fifth of each month. Multiple policies can be drawn from a single bank account.

Policy delivery

On approval of coverage, ODS Alaska will forward the policy, ID cards and any policy amendments directly to the insured within 14 days. ODS Alaska offers a 10-day free look on all coverage; should the insured find that the delivered policy does not meet his or her needs, written instructions from the insured to void the policy must be forwarded to ODS Alaska within 10 days of the policy delivery date. ODS Alaska will refund any premiums. Any request received beyond 10 days will be treated as a policy termination, effective as of the first of the month following the date of receipt.

AKFieldguide.2011

Incomplete application and follow-up process

Applications cannot go to Underwriting until complete with this information.

Application must be updated by the applicant for:

• Height and weight • Missed question on the health statement (1-57) • "Yes" answer to a question (1-57), but no details provided in Section 7 • Details not complete; missed field on condition, treatment or start/end dates • Not signed by all applicants age 18 and over • Signatures not dated, signature date is more than 60 days old or a future date • Business checks will be returned for replacement from a personal checking account

Application must be updated by the producer for:

• No producer signature or date on applications with producer involved • Support personnel signed for appointed producer • Non-appointed producer submission

Individual Sales can collect the following via email or phone from the producer

or applicant and initial by representative. We will contact the producer, if there

is one, for this information:

• Last menstrual period (LMP) • Reason last names are different • Plan selected • Type of application: A = new enrollment, B = addition of dependent, C = upgrade in

• Billing method not selected • Conditional Authorization does not list applicant names, but is signed correctly

The following can be omitted altogether:

• Dental election — presumed no, if no election • SSN of any applicant • Marital status • Business phone • Mailing address and email address • Age • Whether applicant has had ODS Alaska coverage in the last five years • Whether applicant or any family members work for an employer who offers coverage • Waiver or downgrade — presumed no, if no election • Prior coverage credit section

AKFieldguide.2011

ODS Alaska individual application checklist for paper

applications

Section 1: Type of application

□ Type of application is selected

Section 2: Select a plan

□ One medical plan choice is clearly selected □ One dental plan choice is clearly selected, if wanted

Section 3: Applicant information

□ Height and weight for all applicants 19 and older □ First and last name □ Gender □ Date of birth □ Phone number □ Residence address □ Driving history

Section 4: Insurance history

□ The first question must be answered for all applicants 19 and older

Section 5: Prior coverage credit

□ Indicate any prior coverage and attach a copy of the ID card or certificate of credible

Section 6: Health history statement (pages 3 and 4)

□ ALL questions, 1-57, must be clearly and individually marked "yes" or "no" for all

applicants 19 and older

Section 7: Health statement

□ ALL "yes" answers on the health history statement (pages 3 and 4) are clearly

explained and include the question number, dates, condition, treatment, final result and attending physician

□ ALL medications listed under question 56 match up with health conditions on the

health statement

□ Medical providers with current medical records are listed

Section 8: Waivers and downgrades

□ Questions are optional, although will be considered "no" if unanswered

AKFieldguide.2011

Section 9: Agent of record section

□ Agent of record section must be completed, signed and dated

Section 10: Authorization section

□ Applicant names are clearly printed in the box for condition authorization to

use/disclose protected health information, in the middle of the page

□ All applicants age 18 and older have signed and dated the application on the correct

Section 11: Payment options

□ Initial payment option selected □ Subsequent payment option selected □ If auto pay is selected for either the initial or subsequent payments, the auto pay

authorization agreement is completed

□ No business checks are being submitted

AKFieldguide.2011

Source: http://www.odswashington.net/pdfs/ak/uw_field_guide.pdf

ABOUT DRUGS. 0800 77 66 00 TALKTOFRANK.COM FRIENDLY, CONFIDENTIAL DRUGS ADVICE Drugs – lots of them – lots to know about them THINK EVERYONE BC Acid [LSD] Junk [Heroin] Base [Speed] Legal Highs TAKES DRUGS? E Bhang [Cannabis] Liberties [Magic mushrooms]

Journal of Antimicrobial Chemotherapy (2002) 49, 999–1005DOI: 10.1093/jac/dkf009 Risk factors associated with nosocomial methicillin-resistant Staphylococcus aureus (MRSA) infection including previous use of antimicrobials Eileen M. Graffunder* and Richard A. Venezia Department of Epidemiology MC-45, Albany Medical Center Hospital, 43 New Scotland Avenue, Albany,